« A generation after PRIDE’s death, Japan remains the elusive golden goose of MMA | Home | Site with links issues »

The 30 days that changed everything for Bushiroad

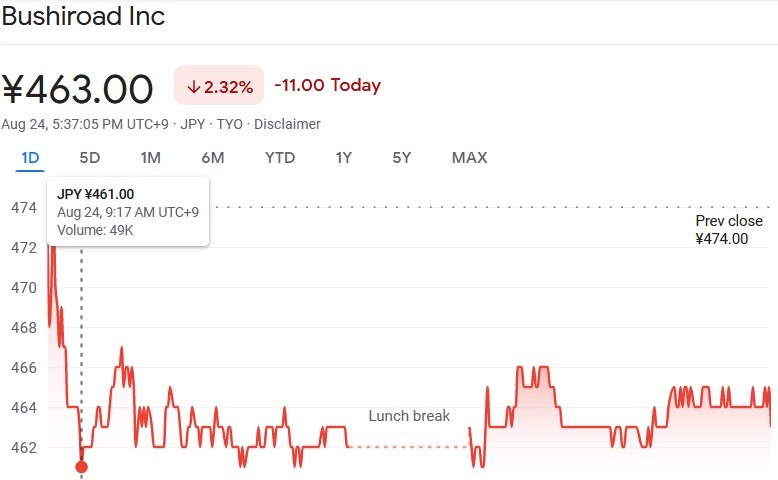

By Zach Arnold | August 24, 2023

How did the biggest player in Japanese professional wrestling experience a 40% plunge in 30 days?

A surface look at what happened to Bushiroad’s stock reveals an ugly collapse that will require aggressive restructuring and growth.

Where things started for the first half of 2023 for Bushiroad

Bushiroad, the publicly-traded parent company of New Japan & Stardom wrestling leagues, experienced some doldrums for an operation listed on the Nikkei’s growth sector. The company had a 52-week high of 960Y ($6.64 USD) a share. A classic upstart publicly traded with some potential for wild swings like you would see in various internet favorites like SOFI.

The difference, of course, is that SOFI is a bank with some really high-end clientele. They yo-yo up and down frequently but have shown signs of life in a delicate economy.

Bushiroad, on the other end, found itself stagnating. Not terribly, but not great either. The company had announced an ambitious four-year plan for wild growth. The sales pitch is entirely built upon the credibility of the quirky Takaaki Kidani, a wrestling nerd of nerds.

The stock dipped around 760Y ($5.25 USD). No big deal. A good financial report and you could easily see things spike to past benchmarks.

The company aggressively decided to change the pricing and scheduling structure for their biggest professional wrestling yearly tournament, the G-1. Mr. Kidani told Tokyo Sports that it was his idea to increase the field to 32 men, with a quarterfinal round of 8 wrestlers, and eventually back-to-back dates at Ryogoku Kokugikan. What also changed was the pricing for tickets and merchandising. A combination of higher merchandise sales plus an appeal to high rollers/hardcores to pay a couple of month’s worth of savings to go to a semi-spot show was a calculated gamble.

The gamble didn’t pay off. A cursory spreadsheet calculation we did on this year’s supersized G-1 CLIMAX 33 tournament estimated around $11 million USD in revenue on gates and merchandising. This is based on $200 USD per spectator with ticket and goods purchase. Exact numbers are not publicly disclosed by the company for all individual events. This is what makes analyzing business tricky for Bushiroad.

Despite a big media push for a new Three Musketeers (Shota Umino, Yota Tsuji, and Ren Narita), it was ultimately Kazuchika Okada vs. Tetsuya Naito in the G-1 33 finals. The tournament was good but not great. What looked ambitious on paper played out conservatively in the end.

What our spreadsheet estimations indicated is that business ticked up a bit in revenue but rising costs and empty seats offset any supersizing attempt to generate higher cash flow to New Japan. What was Mr. Kidani’s motive?

We would soon find out after the G-1 with a shocking financial report.

From the outhouse to the penthouse for Bushiroad

The glow of the G-1 tournament would fade fast.

The Monday after the G-1, Bushiroad stock was trading at 709Y. Not great, but not terrible. But there was a unique curiosity on the stock charts — the volume of trading increased by 4x. Yes, four times more volume on the Monday after the G-1. Over 614,700 shares were traded. The average had been around 150,000 shares traded daily.

Then the first shock hit. Overnight, the stock plunged to 559Y a yen. What happened? Was there a massive dump of shares by institutional players in what’s called the dark pool of stock trading?

After the initial shock to Bushiroad stock, trading Tuesday the 15th (August) was back to regular volume — around 185,500 shares.

Then came the second shock to Bushiroad stock and it was a heart attack. Overnight, the stock dropped to 475Y. The 16th saw massive volume of over 10.6 million shares traded. We’re talking 57 times the level of activity as the previous trading day.

Bushiroad’s stock story changed from the little growth play that could to a gonzo day-trading stock in a hurry.

This chart tells the story (click image for full view):

There been a full trading week with at least each day having 1.3 million shares traded. Things are starting to settle down but the day-trading activity remains volatile. The charts also show a regrettably predictable pattern for investors with diamond hands (click image for full view):

Day-traded penny stocks are vulnerable to wild swings. When a stock is in a downward stage (like a stage 3 plateau or stage 4 collapse), individual traders will attempt to buy on the cheap on the hopes that a lower volume and group think will slowly rise the price up. But before you know it, you got a large block sell and the upwards momentum goes splat. Retail players get hurt.

Why Bushiroad’s stock plunged and it’s negative impact going forward

The financials by Bushiroad last week revealed a company that is doing OK with its wrestling properties but is not generating anywhere near the positive revenue to cover up all the red ink in other corporate departments — like their Digital Contents Unit.

New Japan generated $36 million in revenue for 2022-2023. Stardom generated $10+ million in revenue. Because the girls don’t get paid like the boys, the profit margins are better on the women’s side. Revenue doesn’t equal profit. The total profit from the two operations is a little over $3 million dollars.

A bad sign for Bushiroad is that rising costs are matching their rising revenue totals. Yen fluctuation, travel costs, visa costs, and costs to retain top foreign talent are applying strain to the bottom line.

In response to the released financials, Bushiroad is escalating the prices for wrestling tickets and goods to appeal more to high rollers and hardcore fans. They are selling Tokyo Dome front row tickets for $800 and $1,400. The good news for them is that they have enough fans to pay those absurd prices. Their bigger problem is filling the rest of the seats on big shows. The company is stuck in a “doing OK but not great” mode.

The massive amounts of cash that both WWE and AEW have access to have put New Japan in a very delicate spot to maintain major-level status in the global wrestling picture. They’re more of an influencer inside the business at this point in time.

Bushiroad is trying to extract cash from its current customer base as a top priority. They want to globally expand the brand but find themselves pricing out a lot of potential customers. The internal belief in Bushiroad is that every product they sell is meant to sell other Bushiroad products. You get into anime to sell cards. You get into wrestling to sell merchandise. Everything is about selling another product or leveling up.

The biggest problem for a growth company in a down turn is stock compensation. Not every growth company compensates employees with stock in lieu of cash but most do. It’s treated as income.

Hypothetically speaking, imagine if Bushiroad employees were compensated with stock and the stock went down 40% in value in one week. It’s devastating. Let’s say you have stock that is vesting by the end of the year. How does it change your feeling about buying a new car or what kind of gifts you are buying for family members at Christmas? There are real life consequences to a huge stock plunge for a growth company.

Barring a dramatic turnaround, Bushiroad’s stock is likely going to be stuck in a 10-15% trading range either way until there’s a major financial change. The stock is now increasingly vulnerable to institutional short attacks and, conversely, short squeezes. The wilder the swings, the more volume there is in trading. The higher the volume, the less control you have over operations.

The longer the stock is stuck in quick sand, the more challenging it is going to be to not only hire new management talent but to retain your current employees. Once you start losing key players because of a bad stock situation, you suffer a brain drain.

For Bushiroad’s sake, they need positive developments quickly to maintain the strength of their footprint in the fight business.

Topics: Japan, Pro-Wrestling, Zach Arnold | No Comments » | Permalink | Trackback |